Quick answer: A virtual crypto card is a digital card number issued in seconds — ideal for online purchases, subscriptions, digital advertising, and Apple Pay or Google Pay contactless payments. A physical crypto card is a real plastic card that ships by mail — necessary for ATM cash withdrawals, chip-and-PIN terminals, and merchants that require a physical card for holds (like some hotels and car rentals). For most users in 2026, a virtual card handles 90%+ of spending without the 5-10 day wait for plastic.

This guide compares both options across every dimension that matters — speed, cost, security, acceptance, and specific use cases — so you can make the right choice for how you actually spend.

The Core Difference in One Sentence

A virtual card is a number. A physical card is that number plus plastic, a magnetic stripe, and a chip.

Everything downstream from that single difference — issuance speed, ATM access, replacement time, loss risk, in-person use — flows from whether the card is a set of digits or an object you carry in your wallet.

Side-by-Side Comparison

| Virtual Card | Physical Card | |

|---|---|---|

| Issuance time | Seconds | 5-10 business days (shipped by mail) |

| Cost to issue | Usually free | $5-$25 issuance fee (varies by provider) |

| Online purchases | Full | Full |

| In-person NFC tap-to-pay | Yes (via Apple Pay or Google Pay) | Yes (with contactless terminal) |

| Chip-and-PIN in-person | No | Yes |

| Magnetic stripe swipe | No | Yes |

| ATM cash withdrawals | No | Yes (where supported) |

| Number of cards | Unlimited (on Rivocard) | Usually 1 per account |

| Replacement if compromised | Instant — new card number in seconds | 5-10 business days for new card |

| Risk of physical loss or theft | None | Real — card can be lost, stolen, or skimmed |

| Card freezing | Instant from dashboard | Instant from dashboard (but still need new plastic) |

| Best for | Online, subscriptions, ads, digital services | ATM access, chip-PIN terminals, certain travel holds |

Where a Virtual Card Works

A virtual card works anywhere the card network is accepted and a physical card is not required:

Online shopping. Any e-commerce checkout that accepts Visa or Mastercard accepts a virtual card. Amazon, AliExpress, independent retailers, marketplaces — all work identically. The merchant sees a card number, expiry, and CVV. Whether the card is printed on plastic is irrelevant.

Subscriptions and recurring billing. Netflix, Spotify, Adobe, cloud hosting, SaaS tools — all charge to a stored card on file. A virtual card works for every recurring service. On Rivocard, creating a separate virtual card for each subscription is a useful pattern — if a card is compromised, you cancel that one card without affecting others.

Digital advertising. Google Ads, Meta Ads, TikTok Ads, LinkedIn Ads — all accept Visa or Mastercard for billing. Many digital advertisers and media buyers use virtual crypto cards specifically to fund ad accounts, since it avoids the complications of linking business bank accounts to advertising platforms.

Contactless in-person payments. Add the virtual card to Apple Pay or Google Pay, and you can tap to pay at any NFC-enabled terminal. This covers the vast majority of in-person merchant interactions in 2026 — most modern card terminals are contactless-capable. You do not need plastic to pay in person; you need your phone.

Travel bookings. Flights, hotels booked online, car rentals booked online — all accept virtual cards at checkout. Note: some hotels and car rental companies require a physical card to be present at check-in or pickup for holds (covered below).

App stores and digital content. App Store, Google Play, Steam, PlayStation Store, Xbox — all accept standard card payments. Virtual cards work for every in-app purchase, game, or digital content purchase.

Business expense management. Creating a separate virtual card per vendor or team member gives precise spending control without exposing a primary account. Each card has its own balance, its own history, and can be frozen independently.

Where a Physical Card Is Needed

A physical card is required in a smaller but specific set of situations:

ATM cash withdrawals. This is the primary advantage physical cards hold over virtual ones. If you need local cash — for a market, a taxi, a small merchant that does not accept cards — only a physical card with ATM support gets you there. Virtual cards cannot interface with ATM hardware.

Chip-and-PIN terminals. Some merchants, particularly in certain regions of Europe, still use chip-and-PIN exclusively with no NFC capability. This is increasingly rare in 2026, but it still exists. Only a physical card with a chip handles these terminals.

Hotel check-ins. Many hotels place a hold on your card at check-in — a temporary authorization to guarantee payment for incidentals. Some hotel systems require a physical card to be present (or at minimum the card number to match a physical card that can be produced if needed). Most hotel online bookings accept virtual cards, but check-in policies vary by property.

Car rental holds. Car rental companies typically place a significant hold on the card used at pickup — sometimes $200-$500 or more — and some require the card holder to present the physical card. Prepaid virtual cards are sometimes rejected by car rental companies for this reason, as they prefer cards with a known credit line backing the hold.

Situations where a merchant requires you to show the card. Some merchants — usually in high-value or regulated categories — ask to verify the card physically at the point of service. This is uncommon but does occur.

The Security Comparison

Virtual and physical cards have different security profiles — neither is universally “more secure.”

Virtual card security advantages:

- Nothing to physically lose, steal, or skim at an ATM or POS terminal

- Compromised card number can be replaced instantly with a new number — no wait for plastic

- On Rivocard, you can create a new card number in seconds if one is exposed

- Can be frozen instantly from a dashboard without needing a physical card replacement

- Unlimited cards means you can use a separate card per merchant, limiting exposure

Physical card security risks:

- Can be lost, stolen, or skimmed (magnetic stripe skimming at ATMs or card readers is still a real attack vector)

- Replacement requires waiting for a new card to arrive — typically 5-10 business days

- Chip technology has reduced but not eliminated physical card fraud

What both share:

- PCI DSS-compliant transaction processing

- Standard card-network fraud protections (dispute processes, unauthorized transaction protections)

- 3D Secure (3DS) authentication for online transactions

- Instant freeze from the account dashboard

For most digital-first users, virtual cards are more secure in practice because the attack surface is smaller. The most common card fraud vectors — physical theft, skimming — simply do not apply to a card that has no physical form.

The Cost Comparison

| Cost item | Virtual Card | Physical Card |

|---|---|---|

| Issuance fee | Free (on Rivocard) | $5-$25 at most providers |

| Card funding fee | 5% (deducted from funded amount) | Same |

| Replacement fee | Free (instant, always free) | Varies — may be free or charged |

| ATM withdrawal fee | N/A | Varies by provider and ATM |

| Number you can create | Unlimited | Usually 1 (replacement adds cost and delay) |

For Rivocard specifically: virtual card creation is always free, regardless of how many you create. The 5% fee applies only when you fund a card with balance — not to the act of card creation itself. This makes the Rivocard virtual card model fundamentally different from providers that charge per card or per creation.

Contactless via Apple Pay and Google Pay: Closing the Gap

The most significant gap between virtual and physical cards — in-person usability — has narrowed substantially because of Apple Pay and Google Pay.

Both services allow you to add a virtual card to your phone’s wallet and use it for NFC contactless payments at any merchant with a tap-to-pay terminal. The phone replaces the plastic card for in-person use.

In 2026, the majority of card payment terminals in developed markets support NFC. Major retailers, restaurants, transit systems, gas stations, pharmacies — most have contactless readers. For the large majority of in-person spending situations, a phone with a virtual card loaded into Apple Pay or Google Pay is fully equivalent to tapping a physical card.

The situations where this does not work are the specific edge cases covered above (ATMs, chip-PIN-only terminals, hotel holds requiring physical card presence).

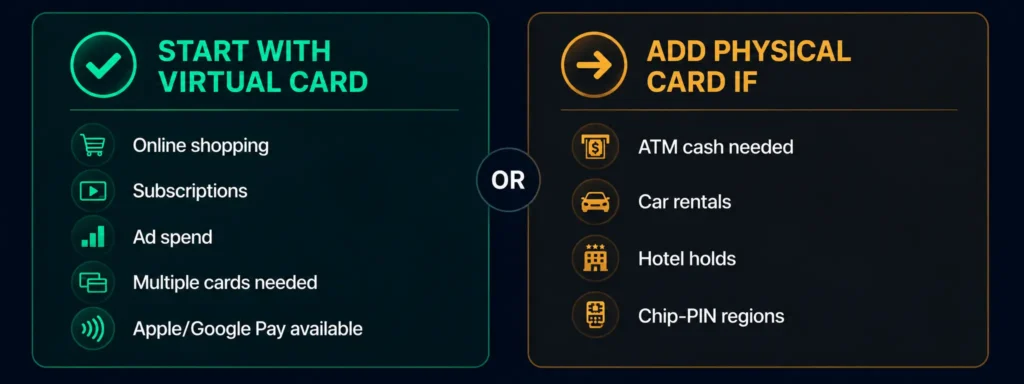

The Decision Framework

Start with a virtual card if:

- You primarily shop online, use digital services, or manage subscriptions

- You want the card available immediately without waiting for mail

- You are a digital advertiser needing a card for ad accounts

- You need multiple cards for different budgets, vendors, or team members

- Your phone has Apple Pay or Google Pay for in-person contactless payments

- You value instant card replacement over plastic

Add a physical card if:

- You frequently need cash from ATMs

- You travel to regions where NFC contactless is not widely available

- You regularly rent cars and the company requires a physical card at pickup

- You stay in hotels that require a physical card at check-in

- You encounter chip-PIN-only terminals regularly in your daily spending

For most users, the recommendation is: virtual card first, always. Assess after a few weeks of use whether your actual spending patterns include enough physical-card-required scenarios to justify ordering plastic. Many users find they do not need a physical card at all.

On Rivocard: Unlimited Virtual Cards, No Physical Card Complexity

Rivocard’s model is virtual-first. The specific advantages this creates:

Unlimited cards at no issuance cost. Create as many virtual cards as your use case requires — one per subscription service, one per ad platform, one for travel bookings, one for general shopping — without paying an issuance fee for any of them. The 5% fee applies only to the balance you put on each card.

Instant issuance. See our full guide on crypto card instant issuance explained for the technical details — but the short version is: your card is ready within seconds of account verification.

No wait for plastic. There is no 5-10 day window where your card exists in manufacturing and postal infrastructure. The card is available immediately.

Instant freeze and replacement. If a card number is compromised, freeze it and create a new one in under a minute. No downtime, no support call, no waiting for new plastic.

For users who need physical card functionality — specifically ATM access — check Rivocard’s current product page for the latest on physical card availability, as product offerings can evolve.

FAQs

What is the main difference between a virtual and physical crypto card?

A virtual card is a card number, expiry date, and CVV that exists digitally — issued in seconds, usable online and via Apple Pay or Google Pay. A physical card is the same information printed on plastic — shipped by mail in 5-10 business days and usable at ATMs, chip-PIN terminals, and any physical card reader.

Can a virtual crypto card be used in person?

Yes — through Apple Pay or Google Pay. Add the card to your phone’s digital wallet and tap to pay at any NFC-enabled contactless terminal. This covers the majority of in-person merchants in 2026. However, it does not work at ATMs or chip-PIN-only terminals that lack contactless readers.

Can a virtual crypto card be used to withdraw cash from an ATM?

No. ATM cash withdrawals require a physical card with a chip or magnetic stripe that can interface with ATM hardware. Virtual card numbers cannot be used at ATMs.

Which is more secure — virtual or physical crypto card?

Virtual cards have a narrower attack surface: nothing to physically lose, steal, or skim. Compromised card numbers can be replaced instantly. Physical cards carry standard plastic fraud risks (skimming, loss, theft) and take 5-10 days to replace. Both use the same underlying payment security standards (PCI DSS, 3DS).

How many virtual cards can I create on Rivocard?

There is no limit. Card creation is always free on Rivocard. You can create and fund as many virtual cards as you need, each with its own balance and independently manageable.

Is there a fee for getting a physical crypto card?

Most providers charge a physical card issuance fee of $5-$25, plus sometimes a delivery fee. Virtual cards are typically free to create. On Rivocard, virtual card creation is always free — check Rivocard’s current product page for physical card availability and fees.

Can I use a virtual crypto card to book hotels and flights?

Yes for online bookings. Most hotel and flight booking platforms accept virtual cards at checkout. Note that some hotels may require a physical card to be present at check-in for holds on incidentals. Book online with virtual, confirm the check-in policy separately.

Do virtual cards work for car rentals?

Virtual cards work for the initial online booking. However, many car rental companies require a physical card (sometimes specifically a credit card, not prepaid) to be presented at pickup for the hold deposit. Confirm the specific rental company’s policy before relying on a virtual card for the full rental process.

How quickly can I get a virtual crypto card compared to a physical one?

A virtual card is issued in seconds — typically within 2-3 seconds of account verification on Rivocard. A physical card takes 5-10 business days to manufacture and ship to your address.

What happens if my virtual card is compromised?

Freeze it instantly from your dashboard. Create a new virtual card with a new number immediately. There is no need to call customer support or wait for a replacement to arrive. On Rivocard, this process takes under a minute.

Get Started

Ready to get your virtual card in seconds? Create your Rivocard account →