Quick answer: Crypto card instant issuance means a virtual card — with a real card number, expiry date, and CVV — is generated and ready to use within seconds of account creation, with no physical manufacturing, no mail delivery, and no activation wait. On Rivocard, instant issuance works because virtual card numbers are generated programmatically by the card issuing infrastructure the moment your account is verified. No KYC is required to trigger issuance. The card is functional for online purchases, Apple Pay, and Google Pay the moment it appears in your dashboard.

If you have ever wondered why some cards take 5-10 business days to arrive while others are available in seconds, this guide explains the full picture — what makes instant issuance possible, what limits it, and why it matters for real-world use.

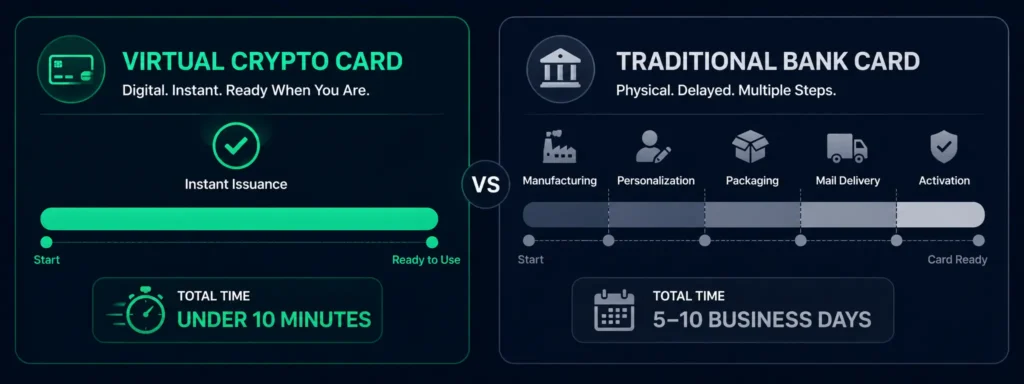

Why Traditional Cards Take Days to Arrive

To understand why instant issuance is significant, it helps to understand what takes so long with traditional cards.

A physical bank card or prepaid card involves:

- Manufacturing: The plastic card has to be physically produced — printed with your name, card number, and expiry date, embedded with a chip and a magnetic stripe

- Personalization: The card data has to be encoded onto the chip and magnetic stripe in a secure facility

- Packaging: The card is inserted into a mailer with PIN information and activation instructions

- Mail delivery: The package goes through standard postal or courier infrastructure — 5 to 10 business days for most providers

- Activation: Upon arrival, most cards require a phone call, online activation, or PIN setup before they work

That entire chain exists because physical cards have physical components. Every step requires time.

A virtual card has none of those steps. There is no plastic, no chip, no magnetic stripe, no mailer, no postal route. A virtual card is a set of numbers — and numbers can be generated programmatically in milliseconds.

What Actually Happens During Instant Issuance

When Rivocard issues a virtual card instantly, here is what happens technically:

1. Account verification triggers card generation. The moment your email is verified, a request is sent to the card issuing infrastructure. This is an API call — essentially, software sending a message that says “generate a new card record for this account.”

2. The card processor assigns a card number. Card numbers are not random. They follow the Luhn algorithm and include a BIN (Bank Identification Number) — the first 6-8 digits that identify the card issuer and network (Visa or Mastercard). The card processor assigns a unique 16-digit number from an available pool.

3. An expiry date and CVV are generated. The CVV is generated cryptographically from the card number, expiry date, and a secret issuer key. It is mathematically derived, not stored in plain text anywhere.

4. The card record is written to the issuer’s system. The card number, expiry, CVV, and associated account details are written to the card management system. From this moment, the card can be authorized at any merchant.

5. The card details appear in your dashboard. Your dashboard displays the card number, expiry, and CVV — typically within 1-3 seconds of account verification.

The entire process from “email verified” to “card ready to spend” takes seconds because it is entirely software-based. No physical process is involved.

Why No KYC Is Needed for Issuance

A common assumption is that identity verification must happen before a card can be issued. This is only partly true — it depends on the card tier and the regulatory framework the issuer operates under.

Rivocard operates on a tiered model:

- Basic tier (no KYC): A virtual card is issued immediately after email verification. This card has spending limits defined by the Basic KYC tier — but within those limits, it is fully functional. No ID required, no selfie, no documents.

- Higher tiers (KYC required): If you want to spend above the Basic tier limits, identity verification is required. Only at that point is KYC triggered.

This is possible because low-value prepaid card programs can operate under simplified due diligence rules in many regulatory frameworks — the risk profile is considered low enough that full identity verification is not required for limited spend. The moment spend thresholds increase, additional verification requirements kick in.

The practical result: you can have a working Rivocard virtual Visa in your dashboard within 2 minutes of visiting the website for the first time, with no documents uploaded.

Instant Issuance vs. Instant Activation

These two terms are often confused — they are not the same thing.

| Instant Issuance | Instant Activation | |

|---|---|---|

| What it means | Card number, expiry, and CVV generated immediately | A pre-existing physical card is enabled for use |

| Physical card involved | No — virtual only | Yes — physical card already exists |

| Why it is fast | Software generates card numbers in milliseconds | Activation toggles a card status flag |

| What the user receives | Complete card details ready to use | A card that was previously inactive |

| Example | Rivocard virtual card after signup | Physical card that arrives in the mail, activated by phone or app |

Instant activation is when you receive a physical card in the mail and then activate it yourself. Instant issuance is when the card itself is created and delivered to you simultaneously, with no physical card ever involved.

What Instant Issuance Enables That Waiting Cannot

The practical difference between instant issuance and traditional card delivery is significant for specific use cases:

Same-day purchases. If you need to make an online purchase today — not in a week — a virtual card issued instantly is the only card-based option. There is no way to speed up physical card manufacturing and delivery to same-day.

Emergency spending access. Travelers who lose a wallet or need a card for a booking that cannot wait have no realistic option with traditional card delivery. A virtual card available in minutes is a genuine solution.

Ad campaign funding. Digital advertisers often need a card ready to fund a new ad account or pay an overdue ad balance immediately. A card that arrives in 7 business days is not useful in this context. An instant virtual card is.

Testing and experimentation. Users who want to try a platform before committing to it benefit from instant issuance — you can evaluate the product in minutes rather than waiting a week for a card that might not suit your needs.

Multiple cards for multiple purposes. On Rivocard, you can create unlimited virtual cards instantly. This enables a workflow that physical cards never could — one card for subscriptions, one for ad spend, one for a specific vendor, each with its own balance and no delivery wait for any of them.

The Security Model Behind Instant Virtual Cards

A question that comes up with instant issuance: if the card is generated so quickly, how is it secure?

Several layers address this:

CVV is dynamically derived, not stored. The CVV is computed from the card number, expiry date, and a private issuer key using a cryptographic algorithm. It is not stored in a database. Even if a card database were compromised, a CVV could not be retrieved — it would have to be recalculated, which requires the secret key.

Card numbers are unique and non-reusable. Each card number is drawn from a specific BIN range allocated to the issuer. Once assigned to an account, it cannot be assigned to another. Card numbers are not sequential in a predictable way.

3D Secure (3DS) adds authentication at checkout. Most merchants now support 3D Secure, which adds an additional authentication step at checkout — a one-time code or biometric confirmation. This means even if a card number were stolen, it cannot be used without passing the 3DS check tied to the card owner’s account.

Instant freeze from the dashboard. If a card is compromised, you freeze it in seconds from your dashboard. A new card with a new number can be created immediately. No need to call a support line, wait on hold, or receive a replacement card in the mail.

PCI DSS-compliant processing. The entire card lifecycle — issuance, storage of card data, transaction processing — operates under PCI DSS standards, the payment card industry’s security framework. This applies regardless of whether the card is physical or virtual.

How Quickly Can You Go from Zero to Spending?

On Rivocard, the realistic end-to-end time from opening the website to completing a first purchase:

| Step | Time |

|---|---|

| Sign up + email verification | ~2 minutes |

| Deposit crypto (USDT TRC-20 recommended) | Deposit initiated in ~2 minutes, confirms in ~1 minute |

| Wallet balance appears | Automatic after confirmation |

| Create and fund virtual card | ~1 minute |

| Card details visible in dashboard | Instant |

| First purchase completed | Depends on checkout process |

| Total | Under 10 minutes |

The only variable is the blockchain confirmation time for your deposit. With USDT on Tron, that is typically under a minute. With Bitcoin, it could be 20-60 minutes. The card issuance itself is always instantaneous.

Instant Issuance vs. Traditional Bank Card Issuance

| Rivocard Virtual Card | Traditional Bank Debit Card | Traditional Prepaid Card | |

|---|---|---|---|

| Time to receive card | Seconds | 5-10 business days | 5-10 business days (mailed) |

| Physical card | No | Yes | Yes (usually) |

| KYC before card | No (Basic tier) | Yes (always) | Usually yes |

| Activation step | None | Usually required | Sometimes required |

| Number of cards | Unlimited | Usually 1-2 | Usually 1 |

| Card replacement if lost | Instant (new virtual card) | 5-10 business days | 5-10 business days |

| Apple Pay / Google Pay | Yes | Yes (usually) | Yes (usually) |

The speed gap is not marginal — it is the difference between minutes and weeks.

What Instant Issuance Does Not Mean

A few clarifications on what instant issuance does not imply:

It does not mean unlimited spending immediately. The card is issued instantly, but the spending limit depends on your account tier. Basic KYC tier limits apply until you complete identity verification.

It does not mean your deposit is instant. The card is issued instantly after account verification. The card balance depends on your crypto deposit, which requires blockchain confirmation. On fast networks (Tron, Solana), this is near-instant. On Bitcoin, it takes longer.

It does not eliminate the need for a balance. An instantly issued card with a zero balance declines at checkout. The card number exists immediately, but spending power requires funding.

It does not mean a physical card is also instant. Instant issuance applies to virtual cards. If you want a physical card (for ATM withdrawals or merchants without NFC), that still requires manufacturing and delivery time.

FAQs

What does instant issuance mean for a crypto card?

Instant issuance means a virtual card — with a complete card number, expiry date, and CVV — is generated and ready to use within seconds, with no physical manufacturing, no mail delivery, and no activation step required.

How fast is Rivocard’s instant issuance?

The virtual card appears in your dashboard within seconds of completing email verification. The card is immediately usable for online purchases. Total time from signup to first purchase is typically under 10 minutes, depending primarily on how fast your crypto deposit confirms on the blockchain.

Do I need to complete KYC before getting an instantly issued virtual card on Rivocard?

No. On Rivocard, a virtual card is issued instantly after email verification — no identity documents required. KYC is only needed if you want to spend above the Basic KYC tier limits.

Is an instantly issued virtual card secure?

Yes. Security does not depend on the speed of issuance. Virtual cards use cryptographically derived CVVs, unique card numbers, PCI DSS-compliant processing, and 3D Secure authentication at checkout. They can also be frozen instantly if compromised and replaced with a new card number immediately.

Can I use an instantly issued virtual card for Apple Pay or Google Pay?

Yes. After your card is funded, you can add it to Apple Pay or Google Pay. This enables contactless NFC payments in person at any merchant with a tap-to-pay terminal.

What is the difference between instant issuance and instant activation?

Instant issuance means a new card number is created and delivered to you immediately — no physical card exists. Instant activation means you received a physical card in the mail and turned it on yourself. They are different processes.

How many virtual cards can I create instantly on Rivocard?

There is no limit. You can create as many virtual cards as you need, each instantly issued and independently funded. Card creation is always free — the 5% fee only applies when you fund a card with balance.

Can instantly issued virtual cards be used internationally?

Yes. Virtual cards run on the Visa network, which is accepted at merchants globally. Rivocard charges 0% on international transactions — no foreign transaction surcharge applies regardless of where the merchant is located.

What happens if my instantly issued virtual card is compromised?

Freeze it instantly from your Rivocard dashboard. Create a new virtual card immediately with a new card number. No wait for a replacement to arrive in the mail, no downtime, no support call required.

Get Started

Ready to get your virtual card in seconds? Create your Rivocard account →