Quick answer: A crypto prepaid card lets you load cryptocurrency onto a card account, where it’s converted into regular currency — either the moment you spend or ahead of time when you top up. Once that balance is on the card, you spend it anywhere the card network (usually Visa or Mastercard) is accepted, online or in person, without needing a separate bank account or manually cashing out your crypto first.

That’s the one-sentence version. Here’s what’s actually happening at each step, because the mechanics matter — they’re the difference between a card that works smoothly at checkout and one that leaves you standing at a register wondering why your payment just failed.

What a Crypto Prepaid Card Actually Is

A crypto prepaid card isn’t a credit card, and it’s not quite a debit card either. There’s no credit line, and it isn’t directly wired to a traditional bank account. Instead, it’s a prepaid balance — like a gift card — except the balance is funded with crypto instead of cash.

You load value onto it before you spend, the issuer converts that value into spendable fiat currency, and the card itself runs on standard payment rails (Visa or Mastercard), so merchants treat it exactly like any other card. They have no idea crypto was ever involved — to a coffee shop terminal, your tap is indistinguishable from someone paying with a regular debit card.

Why Crypto Prepaid Cards Exist in the First Place

It’s worth understanding the problem this solves, because it explains why the product is built the way it is. Crypto, by design, isn’t accepted at the vast majority of physical and online merchants. To turn it into something spendable, you’d traditionally need to: sell it on an exchange, wait for the fiat to settle, withdraw to a bank account, and then spend from that account — a process that can take days and usually involves more than one fee.

A crypto prepaid card collapses that entire chain into one step. The conversion happens inside the card platform itself, so the gap between “I have crypto” and “I can buy something with it” shrinks from days to minutes.

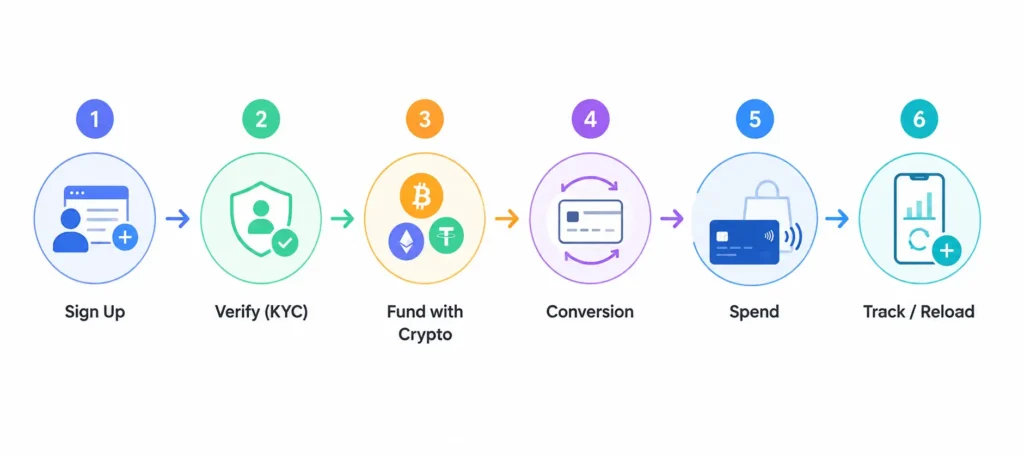

The Step-by-Step Process

1. Choose a provider and create an account. Not all crypto card issuers operate the same way — some are tied to a specific exchange, others operate independently. You sign up, complete identity verification (KYC), and get issued a virtual card instantly, with a physical card optionally mailed afterward.

2. Verification (KYC) happens before you can fund anything. This step exists because card issuers are regulated financial entities, not just crypto wallets — they’re subject to the same Know Your Customer and Anti-Money Laundering obligations as banks. Expect to submit a government ID and basic personal details. This isn’t optional friction the provider added for fun; it’s a legal requirement for issuing a card linked to a payment network.

3. Fund the card with crypto. You send crypto from your own wallet or exchange to the address the platform provides. Depending on the provider, supported assets typically include major coins like BTC, ETH, and USDT, though the exact list varies by issuer — always check the live supported-assets page rather than assuming.

Want the full walkthrough? See our step-by-step guide to fund your card with crypto — including the network mistakes that cost first-time users money.

4. Crypto-to-fiat conversion happens. This is the step most explanations skip, and it’s the one that actually determines how your card behaves. There are two models in use across the industry:

| Pre-Funded Conversion | Real-Time Conversion | |

|---|---|---|

| When conversion happens | The moment crypto lands | At the moment of each purchase |

| Balance behavior | Fixed fiat number once converted | Fluctuates with live exchange rate until spent |

| Price certainty | High — locked in immediately | Lower — depends on market at checkout |

| Best for | Users who want predictable spending power | Users comfortable tracking market movement |

Neither model is “better” universally. What matters is knowing which one your card uses, because it changes how you should think about when to load funds.

5. Spend like a normal prepaid card. Once converted, the balance behaves exactly like money on any prepaid Visa or Mastercard: tap to pay, swipe, insert chip, pay online, add to Apple Pay or Google Pay. The merchant’s payment terminal has no crypto-awareness whatsoever — it just sees a valid card number and an available balance.

6. Track, reload, and manage. From your account dashboard or app, you can see balance, transaction history, and reload whenever you run low — repeating steps 3–4 each time.

How Long Does Conversion Actually Take?

This depends on blockchain confirmation time, not the card issuer — and it varies meaningfully by network:

- Bitcoin: Block times run roughly 10 minutes, and most platforms wait for multiple confirmations before crediting funds, so this is typically the slowest option.

- Ethereum: Block times are closer to 12 seconds, with funds usually recognized faster than Bitcoin.

- Tron-based USDT: Often the fastest practical option for stablecoin transfers, with confirmations typically landing in seconds and minimal network fees.

If speed matters to you — say, you’re funding the card right before a purchase — this is a genuinely useful thing to know before you pick which asset to send.

Common Mistakes First-Time Users Make

- Sending the wrong asset to the wrong network. Sending USDT on the wrong blockchain (e.g., the wrong “version” of USDT) to an address expecting a different network is one of the most common — and costliest — crypto mistakes. Always double-check the network matches what the platform specifies.

- Assuming the balance updates instantly. It updates once the network confirms the transaction, not the second you hit send.

- Not understanding which conversion model they’re using. This causes confusion when a balance doesn’t match what someone expected based on a price they saw earlier.

- Ignoring foreign transaction fees while traveling. These are a card-network-level fee, separate from crypto conversion, and easy to overlook.

Pros and Cons, Honestly

Advantages:

- No traditional bank account required

- Spend crypto anywhere Visa/Mastercard is accepted — already a near-universal network

- Conversion happens in one step instead of a multi-day exchange-to-bank chain

- Works for both online and in-person purchases

Trade-offs to know going in:

- KYC verification is mandatory, not optional

- Conversion model (pre-funded vs. real-time) affects how predictable your spending power is

- Network confirmation times mean funding isn’t always instant

- Tax treatment of crypto-to-fiat conversion varies by country and isn’t something the card handles for you

Crypto Prepaid Card vs. Crypto Debit Card

These terms get used interchangeably, but they’re not identical. A prepaid card draws only from a balance you’ve loaded in advance — you can’t spend more than what’s on it. A debit card is typically linked to an ongoing account that can pull funds more dynamically, sometimes directly from a connected exchange balance in real time. We break this down in full in our crypto prepaid card vs. crypto debit card comparison.

Crypto Prepaid Card vs. a Regular Prepaid Card

A regular prepaid card is funded with cash or a bank transfer — there’s no conversion step at all. A crypto prepaid card adds exactly one extra layer: the crypto-to-fiat conversion described above. Everything downstream — how you spend it, where it’s accepted, how refunds work — functions identically to a standard prepaid card once that conversion is complete.

Who Actually Uses These Cards

In practice, a few user types show up repeatedly:

- People paid in crypto (freelancers, contractors, remote workers) who need a fast path from “crypto income” to “everyday spending” without routing through a bank.

- Travelers and digital nomads who want to carry spending power without juggling multiple currencies or relying on local banking infrastructure.

- Crypto holders who want to spend without fully cashing out through a traditional exchange-to-bank withdrawal.

- Privacy-conscious spenders who prefer not to link every purchase directly to a personal bank account.

Is It Safe to Use?

Reputable issuers combine KYC verification, encryption, and PCI DSS–compliant card processing — the same standard banks and major card networks use. Card-network protections (like dispute processes for unauthorized transactions) generally apply the same way they would on any other Visa or Mastercard product, since the conversion to fiat happens before the card network ever sees the transaction. If security is your main hesitation before signing up, it’s worth reading in detail rather than taking it on faith. Rivocard Security is our top priority.

FAQs

Do I need a bank account to use a crypto prepaid card?

No. The card itself functions as your spending account — that’s the entire point of the prepaid model. You only need a crypto wallet or exchange account to fund it.

Is converting crypto to a card balance a taxable event?

In many jurisdictions, converting crypto to fiat is treated as a disposal event for tax purposes, which can trigger capital gains or losses. Rules vary significantly by country, so this isn’t something to guess on — confirm your specific obligations with a tax professional.

How long does it take for crypto to show up on my card?

It depends on the blockchain network’s confirmation time, not the card issuer — some chains confirm in seconds, others take longer during periods of congestion. See the network comparison above for typical ranges.

Can I use a crypto prepaid card internationally?

Yes, anywhere the underlying card network (Visa/Mastercard) is accepted, which is the vast majority of merchants worldwide. Foreign transaction fees may apply depending on the issuer.

What happens if the crypto market moves while my balance is loading?

With pre-funded conversion, your balance is already locked in fiat, so market movement afterward doesn’t affect it. With real-time conversion, your spending power can shift until the moment you actually transact.

Can I lose money to network fees when funding the card?

Yes — sending crypto on-chain involves a network fee paid to miners/validators, separate from anything the card issuer charges. Faster, cheaper networks (like Tron for USDT) typically minimize this.

What happens if I send the wrong cryptocurrency or use the wrong network?

This is usually unrecoverable. Crypto transactions sent to the wrong network or asset type are typically not reversible, which is why double-checking the deposit details before sending is essential.

Do crypto prepaid cards have monthly fees?

This varies by issuer — some charge account or maintenance fees, others don’t. Always check the live fees page for current, accurate numbers rather than relying on general assumptions.

Ready to see it in action? See how Rivocard’s card creation works →