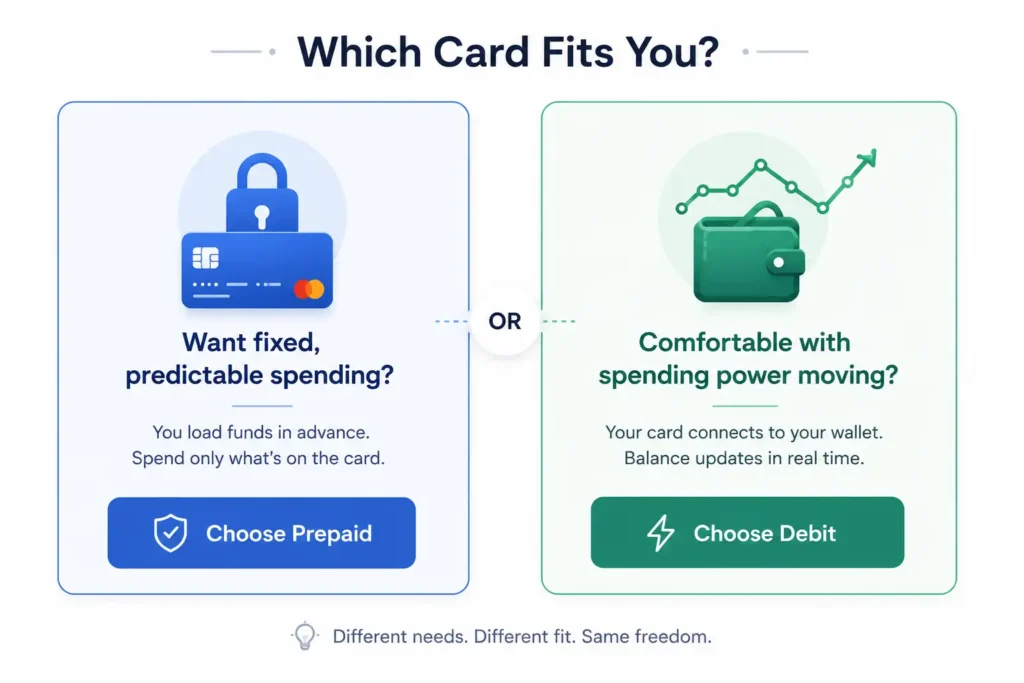

Quick answer: A crypto prepaid card only spends a balance you’ve already loaded and converted in advance — you can’t spend more than what’s on it. A crypto debit card stays linked to an ongoing crypto wallet or account, and typically converts crypto to fiat in real time at the moment of each purchase. The prepaid model gives you predictability; the debit model gives you flexibility — but each comes with trade-offs worth understanding before you pick one.

At a Glance

| Crypto Prepaid Card | Crypto Debit Card | |

|---|---|---|

| Funding | Load crypto in advance; converts to a fixed fiat balance | Stays linked to your crypto wallet/account balance |

| When conversion happens | Ahead of time, when you top up | Typically at the moment of purchase |

| Spending limit | Exactly what you’ve loaded — no more, no less | Tied to your current wallet balance, which can fluctuate |

| Price exposure | None after loading — balance is locked in fiat | Ongoing — your spending power moves with the market until you spend |

| Account relationship | Standalone balance, not linked to an ongoing account | Linked to a persistent wallet/account |

| Best for | Predictable budgeting, gifting, controlled spending | Users who want to spend directly from holdings without a separate load step |

If you’ve read our guide on how a crypto prepaid card works, you already understand the prepaid side. This article focuses on what changes when you compare it to the debit model.

What Makes It a “Prepaid” Card

The defining trait of a prepaid card — crypto or otherwise — is that spending power is capped by what you’ve already loaded. There’s no live connection back to your wallet at the moment of purchase. You fund it, it converts, and from that point forward the balance behaves like a gift card: fixed, predictable, and disconnected from whatever the market does next.

This matters most for budgeting and control. If you load $200 worth of crypto onto a prepaid card, you can spend exactly $200 — not a cent more, regardless of what the market does in the meantime, and not a cent less unless fees apply.

What Makes It a “Debit” Card

A crypto debit card works differently under the hood. Instead of a fixed, pre-converted balance, it stays connected to your live crypto wallet or exchange account. When you make a purchase, the issuer typically sells the equivalent amount of crypto at that moment, converts it to fiat, and sends payment to the merchant — all within seconds, automatically, without you manually “loading” anything beforehand.

The practical effect: your spending limit isn’t a fixed number you set in advance — it’s whatever your wallet happens to be worth right now. If your crypto holdings are worth $500 today and $480 tomorrow because of a market dip, your spending power moved with it, without you doing anything.

The Real Differences That Matter

1. Price exposure timing. This is the single biggest functional difference. With a prepaid card, you accept the conversion rate once, at load time, and you’re done — the market can do whatever it wants afterward and your balance doesn’t change. With a debit card, you’re exposed to the market price at the literal moment of every single purchase, which means the “cost” of your coffee in crypto terms shifts daily even if the menu price never changes.

2. How “running out” works. A prepaid card simply declines once the loaded balance hits zero — clean and predictable. A debit card’s available balance is recalculated continuously based on your wallet’s current market value, so a transaction that would have gone through yesterday might get declined today purely because the market moved against you, even if you didn’t spend anything in between.

3. The account relationship. A prepaid card is intentionally disconnected — once loaded, it doesn’t matter what happens to your original wallet. A debit card keeps that connection alive permanently, which is convenient (no separate top-up step) but also means your spending card is only as available as your wallet’s current balance and your provider’s uptime.

4. Fee structure tendencies. Conversion fees apply differently depending on the model. Prepaid cards typically charge a conversion fee once, at load time. Debit cards may apply a (sometimes smaller, sometimes comparable) conversion fee on every single transaction, since every purchase triggers a fresh crypto sale. Exact figures vary significantly by issuer — always check the live fees page rather than assuming either model is cheaper by default.

5. KYC and setup depth. Both models require identity verification as a baseline regulatory requirement, but debit-style products that maintain an ongoing account relationship sometimes carry additional verification tiers tied to higher spending limits, since the issuer is taking on more ongoing exposure than with a one-time prepaid load.

Pros and Cons, Side by Side

Crypto Prepaid Card

Pros:

- Spending power is fixed and predictable once loaded

- Zero price exposure after conversion

- Easier to use for strict budgeting or gifting

- Simpler mental model — what you loaded is what you have

Cons:

- Requires a manual top-up step before you can spend

- If you load too little, you have to reload before continuing

- Locked-in conversion rate means you don’t benefit if the market moves in your favor afterward

Crypto Debit Card

Pros:

- No separate “loading” step — spend straight from your wallet

- Spending power can grow if your holdings appreciate

- Convenient for users who want a persistent connection to their crypto balance

Cons:

- Spending power fluctuates with the market, sometimes unpredictably

- A transaction can be declined due to a price dip even if your crypto quantity hasn’t changed

- Tracking your actual remaining “budget” in fiat terms is harder, since it’s a moving target

Which One Should You Actually Choose?

This comes down to how you think about money, not which product is objectively “better.”

- Choose prepaid if you want a fixed, predictable spending amount — useful for monthly budgeting, travel spending money, or simply not wanting your card balance to be affected by crypto volatility once it’s loaded.

- Choose debit if you’re comfortable with your spending power moving alongside the market, and you’d rather skip the manual top-up step entirely.

Neither is “safer” in a security sense — both rely on the same KYC, encryption, and card-network protections. The difference is purely about how much price exposure and manual control you want.

A Common Misconception

These terms get used interchangeably online — partly because both ultimately let you “spend crypto,” and partly because some providers blur the line by offering auto-reload features that make a prepaid card behave almost like a debit card. If a provider advertises “auto top-up,” check carefully which model actually applies: a card that auto-reloads from your wallet when the balance runs low is functionally closer to a debit card than a pure prepaid one, regardless of what it’s marketed as.

FAQs

Is a crypto prepaid card safer than a crypto debit card?

Not inherently — both typically rely on the same KYC verification, encryption, and PCI-compliant processing. The prepaid model limits your financial exposure (you can’t lose more than what’s loaded), but that’s a budgeting safeguard, not a security difference.

Can I lose money on a crypto debit card if the market drops?

You don’t lose money you’ve already spent, but a market drop can reduce your available spending power for future purchases, since your balance is tied to current wallet value rather than a fixed fiat amount.

Do crypto prepaid cards have lower fees than crypto debit cards?

It depends entirely on the issuer — some prepaid cards charge a single conversion fee at load time, while some debit cards charge per-transaction. Always compare actual published fee schedules rather than assuming one model is cheaper by default.

Can a crypto debit card decline a purchase even if I have enough crypto?

Yes, if the market value of your holdings drops below the purchase amount at the moment of the transaction, even if the crypto quantity itself hasn’t changed.

Which is better for traveling?

Prepaid cards are often preferred for travel since the spending amount is locked in before you leave, removing the risk of market swings affecting your budget mid-trip.

Can I have both types of cards?

Yes — many crypto holders use a prepaid card for predictable day-to-day budgeting and keep a separate connection to their main holdings for larger or more flexible spending.

Not sure which fits your spending style? See why Rivocard’s approach works →